| ▲ | CSMastermind 2 days ago |

| A currency being worth half it's value in 25 years is absurd. The US despreately needs to make it's money a stable unit of measure. |

|

| ▲ | nonethewiser 2 days ago | parent | next [-] |

| In some sense it's absurd. But historically its normal. And to be more precise, 25 years to halve is actually less inflation than the historical average of 3.29% from 1914-2025. At that rate it would take 21-22 years to halve. Actually there is a surprisingly good trick to be able to calculate this called the rule of 72. Take the inflation percentage (2, 3 %) and divide 72 by it. Thats how many years it will take to halve. Not completing accurate but actually very close. But yeah, inflation is a bitch over long time horizons. It makes me laugh when people say stocks are risky. Say you are 20 years old and want to save $2M USD for your retirement by 65. Expect that to be more like $470k. |

| |

| ▲ | sudo_gopnik 2 days ago | parent | next [-] | | Historically - it's actually NOT normal. Link and quote below that examines this with graphs but, the crux is that we have accepted higher inflation in order to achieve stable inflation that is predictable. "For the pre-Fed period (1790-1913), the average annual inflation was 0.4 percent with a coefficient of variation of 13.2. During the period 1941-2016, these figures changed to 3.5 percent and 0.8, respectively. If we look at the post-Volcker era (1988-2016), annual inflation was 2.2 percent on average with a coefficient of variation of 0.4." - Source: https://www.stlouisfed.org/publications/regional-economist/s... Also recommend Debt: The First 5000 Years (David Graeber) and Capital in the Twenty-First Century (Thomas Piketty) which cover this and more on how current concepts of finance and capital post-1914 are incredibly different from the majority of human civilization. I think a broader historical/anthropological approach is helpful here to understand why those tradeoffs were made. | | |

| ▲ | Aurornis a day ago | parent [-] | | > "For the pre-Fed period (1790-1913), the average annual inflation was 0.4 percent with a coefficient of variation of 13.2. During the period 1941-2016, these figures changed to 3.5 percent and 0.8, respectively. If we look at the post-Volcker era (1988-2016), annual inflation was 2.2 percent on average with a coefficient of variation of 0.4." - Citing an average number is misleading since the chart of the value of a dollar during that time looks like a zig-zag with some massive swings in both directions. This means periods of severe deflation, too, which can be very bad for people. It definitely was not flat or consistently near zero, though citing an average number is a great way to give that impression. | | |

| ▲ | wredcoll a day ago | parent | next [-] | | Maybe a better metric is some kind of yearly median, i.e what you would actually experience living year by year. | |

| ▲ | dragonwriter a day ago | parent | prev [-] | | > Citing an average number is misleading Not when you are also citing the coefficient of variation it isn’t. > since the chart of the value of a dollar during that time looks like a zig-zag with some massive swings in both directions. Uh, exactly the claim made, “we have accepted higher inflation in order to achieve stable inflation that is predictable.” (emphasis added) Characterizing this as a bad thing is, IMO, quite bonkers, but so is denying that it is exactly what has happened. |

|

| |

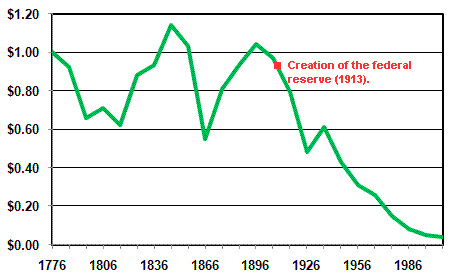

| ▲ | mothballed 2 days ago | parent | prev | next [-] | | If you move to before the central bank was created in 1913, the dollar remained remarkably stable in relation, although it did oscillate, it never deviated more than 50% from the starting point until after creation of the fed. https://upload.wikimedia.org/wikipedia/commons/c/c7/Dollar_v... | | |

| ▲ | somenameforme 2 days ago | parent | next [-] | | What is the source of data that image is using? It seems odd. A datum I quite like is the Campbell's Tomato Soup Inflation Index. [1] Since their introduction in 1897, Campbell's has sold the same tomato soup in the same size container. Its price remained quite stable until 1971 at which point it went into loony land, like many other data. [2] The point is that even after the central bank was introduced, the US remained on a literal or defacto gold standard, of varying sorts, until 1971. That's when Bretton Woods ended and the value of the USD became based on absolutely nothing and the government granted themselves the power to 'print' arbitrary amounts at their discretion. [1] - https://theglitteringeye.com/the-tomato-soup-index/ [2] - https://wtfhappenedin1971.com/ | | | |

| ▲ | woodruffw 2 days ago | parent | prev [-] | | It seems difficult to draw any inference from this, given how different the US’s economy and global position is in 2025 versus 1913. | | |

| ▲ | gbacon 2 days ago | parent | next [-] | | Lots of topics that we discuss on HN require careful thought and other difficult efforts but somehow do not extinguish our curiosity. Going back to the ancient Romans, an ounce of gold has always been able to purchase a suit of clothes. As the market becomes more efficient at producing goods and services, we should expect prices to decrease, not inflate. In some sectors, we do see this outcome but not in others. Yes, the analysis required to explain why is difficult, and perhaps more difficult is having to face conclusions that challenge one’s priors. | | |

| ▲ | woodruffw a day ago | parent [-] | | There’s a big gap between curiosity and making inferential leaps. > As the market becomes more efficient at producing goods and services, we should expect prices to decrease, not inflate. Yes, that’s why the cost of clothes has decreased in real terms. |

| |

| ▲ | mothballed 2 days ago | parent | prev [-] | | ... I was directly addressing GGP using 1914 as a cutoff. Now you object to the cutoff I didn't introduce only when someone introduce data on the other side of it? Funny how that magically ends up being the case. | | |

| ▲ | woodruffw 2 days ago | parent [-] | | To be clear, I think it’s also hard to make inferences after 1913. But it’s easier (and particularly after 1945, 1971, etc.) because the US’s geopolitical status after those periods is at least analogous and a matter of econometric research. | | |

| ▲ | mothballed a day ago | parent [-] | | The period from 1776-1913 arguably had as many changes as the period from 1913 to 2025. In the first 130 years of the US, the value of the dollar didn't change, as far as I can tell, more than 50% from the starting point. From 1913 to 2025, the dollar lost 96+% of its value. The difference between a ratio of 2:1 and a ratio of more like 30:1. | | |

| ▲ | woodruffw a day ago | parent [-] | | > The period from 1776-1913 arguably had as many changes as the period from 1913 to 2025. I'm not arguing it didn't. But I think in kind the US's global economic position didn't change substantially between full independence in 1783 and 1913. It grew during that period, but the idea of the US as a peer (and then dominant) economic world power is a distinctly post-WWI one. | | |

| ▲ | mothballed a day ago | parent [-] | | Why do you believe that makes the data comparison pre to post central bank irrelevant? |

|

|

|

|

|

| |

| ▲ | Pooge 20 hours ago | parent | prev | next [-] | | > It makes me laugh when people say stocks are risky. I agree 100% with your thought. However, I've come with an explanation: people save $100k and the amount in itself will not budge unless they use that money. This, of course, is a flawed argument as the amount doesn't matter; what you can buy with it does. With stocks—I prefer ETFs but I digress—you do not know the amount you will have in 40 years (even if, historically, you would have made money in absolutely all cases). This uncertainty, coupled with lack of economics knowledge, is why people qualify stocks as "risky". However, instead of "risky", I think they mean "volatile". Cash is absolutely the riskiest of assets as it loses value in 100% of cases despite being more stable than stocks. And my cynic mind tells me that the banking industry has all to gain from telling people that "stocks are very risky", instilling fear and, instead, selling them over-complicated products where the bank is guaranteed to make a profit on the back of their clients. Of course, they tell them it's "100% safe". | |

| ▲ | gbacon 2 days ago | parent | prev | next [-] | | Your starting point of 1914 is strangely specific. Why did you choose it? | |

| ▲ | rkowalick 2 days ago | parent | prev | next [-] | | The correct calculation isn’t too hard either. If currency halves in purchasing power in 25 yrs, that means inflation is 100% in 25 years, so (1 + r)^25 = 2

r = 2^(1/25) - 1 ~ 2.8%

| | | |

| ▲ | jollyllama a day ago | parent | prev [-] | | A span of time that happens to include The Great Depression. |

|

|

| ▲ | joshuamcginnis 2 days ago | parent | prev | next [-] |

| We're $38.8 trillion in debt and still printing. https://www.usdebtclock.org/ |

| |

| ▲ | kristofferR 2 days ago | parent [-] | | Inflation is just what you want when your debt is denominated in the currency that is being inflated, though. The more inflation the easier it will be to service the debt. | | |

| ▲ | 2 days ago | parent | next [-] | | [deleted] | |

| ▲ | BartjeD 2 days ago | parent | prev [-] | | That's why everyone sane is fleeing into gold and silver. | | |

| ▲ | mothballed 2 days ago | parent | next [-] | | They're probably too late, it's already priced in. Gold is up like 30% in 3 months. | | |

| ▲ | nonethewiser 2 days ago | parent [-] | | Being up doesnt show that it's priced in. | | |

| ▲ | mothballed 2 days ago | parent [-] | | Of course not. It being known to the market is what causes it to be priced in. | | |

| ▲ | lesuorac a day ago | parent [-] | | Thanks, I'll go short gold now since it's going to go down! Things being priced in is such horse shit. Momentum trading works specifically because the market fails to price in information. | | |

| ▲ | jart a day ago | parent | next [-] | | It's a foolish idea to short gold on the eve of a currency crisis. Gold went up 1812% the last time this happened. You'll be paying through the nose if you do it with $GLD since it's hard to borrow. You'll get IV crushed if you do it with put options. The smart way to profit off gold's fall from grace is by selling futures each time it hits a new high and then closing your position quickly after the inevitable ~50 point pullback. Markets can be timid. They sometimes price in new information slowly and reluctantly. | |

| ▲ | a day ago | parent | prev [-] | | [deleted] |

|

|

|

| |

| ▲ | 2 days ago | parent | prev [-] | | [deleted] |

|

|

|

|

| ▲ | mdnahas 19 hours ago | parent | prev | next [-] |

| Economist here. No, you don’t want that. Inflation is annoying, but deflation is destructive. When that happens, people hold on to money as an investment and it doesn’t flow in the economy. The Great Depression was caused by deflation. (See Milton Friedman and Anna Schwartz’s A Monetary History of the US.) As a result, central banks try to have a little inflation, so that random mistakes don’t push us into deflation. The Fed’s target is 2%. I think it should be a little higher. (See Fischer Black’s “Interest Rates as Options” and the shadow short-term rate.) No one should be holding inflating dollars over the long term. That money should be invested in loans (bonds, mortgages, …) or equity (stocks, real estate, …). We have good ways of comparing investments over time by removing the inflation. These are CPI or the GDP deflator. |

| |

| ▲ | mdnahas 19 hours ago | parent [-] | | P.S. Half its value over 25 years is extremely stable if you look at the history of money, especially fiat money. It halved in value in 9 years, from 1974 to 1983. |

|

|

| ▲ | silisili 2 days ago | parent | prev | next [-] |

| We tend to target 2% inflation. Half in 25 years is under 3%, so on target. That said, I feel like this number is way off, personally, based on changes in housing and food prices between the two times. |

| |

| ▲ | nonethewiser 2 days ago | parent [-] | | Certainly a lot of that inflation was in the last ~8 years. I certainly know what you mean. Groceries are one of the more discretionary items. Your mortgage is fixed, demand for gas is inelastic, etc. But groceries you respond to the price. And so many staples have become 2,3,4X times more expensive compared to pre-covid. I remember the cheap beef (chuck roast) was about $4/lb and decent steak (ribeye) was about $9/lb. Now its about $10/lb and $22/lb. So psychologically, now your "splurging" just gets you the "cheap" stuff. Wages have risen a bit. But 1) not nearly as much as inflation 2) these are very asymetric and 3) the way they rise doesnt feel like wage inflation. Even those who saw wages rise due to inflation probably felt like it was other things. Such as simply changing jobs. Or just normal yearly review. Or maybe they havent switched jobs and have some "unrealized gains" awaiting them still. No one one saw their wages incrementally rise month by month. | | |

| ▲ | silisili 2 days ago | parent [-] | | I think wages are a great way to look at it too, rather than just comparing prices. Said another way, I think making 100k in 1995 would make one feel way, way richer than making 200k today. | | |

| ▲ | lotsofpulp 2 days ago | parent [-] | | How you feel is also very geographically dependent, and quality of life dependent. The government published nationwide inflation measures are completely irrelevant to anyone who had a goal of buying land in a tier 1 metro, or in the higher end suburbs of tier 2 metros. And you will feel very different based on if you have kids or not. Land, healthcare, and education pretty much eclipse everything else. |

|

|

|

|

| ▲ | crazygringo a day ago | parent | prev | next [-] |

| It's not absurd. And there's no automatic way to make money perfectly stable. That's not how money works. And deflation is much worse. So we target a small 2% yearly inflation so that if it's 1% or 3% it's not a big deal. Whereas if you target 0% and wind up with -1%, you've got problems. |

| |

| ▲ | jart a day ago | parent [-] | | There's that word we again. So you're the crazy gringo who always picks my pocket? Deflation is only bad for people who hold a lot of debt. For people who are cash positive, deflation means you're richer, you're being paid more to do the same job, etc. all while maintaining your freedom. Deflation actually being good is the central gamble behind bitcoin's design. If more people understood that then they'd probably stop using it for such frivolous purposes. Not everyone is privileged enough to even hold debt, so it's really an exclusionary system. And what do the people who the system trusts to have debt (e.g. private equity firms) do with it? They do leveraged buyouts to rip out the heart and soul of responsible American companies. The only thing inflation is good for is keeping folks running on the hamster wheel and bankrolling entitlements. | | |

| ▲ | woodruffw a day ago | parent | next [-] | | > Not everyone is privileged enough to even hold debt, so it's really an exclusionary system This seems backwards: I think the most salient debt in the average American consumer's life is student loans, car loans, credit card debts, mortgages, etc. These aren't hallmarks of privilege; not having any of them would be the hallmark. (You might be right about corporate debt, I don't know. But I do think "deflation is only bad for people who hold a lot of debt" does a disservice in suggesting that that isn't a lot of ordinary people.) | | |

| ▲ | jart a day ago | parent | next [-] | | So you think being a carless renter with no formal education or credit cards is privileged? I thought privileged people called them rubes. | | |

| ▲ | woodruffw 17 hours ago | parent [-] | | I’m pretty sure I’m saying the exact opposite of that. The point was that debt doesn’t map cleanly onto privilege at all. (Notably, the credit industry has moved onto schemes like BNPL that target individuals who would otherwise be protected from predatory credit by consumer protection laws. Those people are exploited, and unambiguously benefit - albeit not much - from an inflationary instead of deflationary environment.) |

| |

| ▲ | necovek a day ago | parent | prev [-] | | I think you missed their point: you are referring to the American middle class, but really, there are people much poorer who couldn't even go to university, or get out of an apartment rental in lousy neighbourhood, or own a crappy $500 car or... | | |

| ▲ | woodruffw 17 hours ago | parent [-] | | Those people frequently have even more exploitative forms of debt, like BNPL and payday schemes. |

|

| |

| ▲ | dogmayor 18 hours ago | parent | prev [-] | | Short-term deflation can be beneficial for some, but sustained deflation leads to a downward spiral that harms all. A lower cost of goods is great until it causes reduced aggregate investment and demand, which in turn can lead to wage reductions and layoffs. It's also harder to navigate out of a deflationary environment. Deflation isn't desirable in the long run. |

|

|

|

| ▲ | pinkmuffinere 2 days ago | parent | prev | next [-] |

| Why??? My (very limited) understanding is that we like a small amount of inflation, to incentivize reinvestment into the economy/R&D/etc. If there’s no inflation, you incentivize dragon-hoarding behavior |

| |

| ▲ | jsbg 2 days ago | parent | next [-] | | that's why no one every buys TVs | | |

| ▲ | wredcoll a day ago | parent [-] | | honestly its a large factor for me personally when I look at buying a new tv! |

| |

| ▲ | gweinberg a day ago | parent | prev [-] | | Your understanding is silly. Inflation or no inflation, you'd like to maximize your roi. | | |

| ▲ | pinkmuffinere a day ago | parent [-] | | In your bank account, do you hold cash? If inflation was higher, say at 10,000%, would you hold less cash? For many people the answer is yes, which shows that higher inflation incentives reinvestment |

|

|

|

| ▲ | mothballed 2 days ago | parent | prev | next [-] |

| Get a brokerage account that has a sister bank account. Put money in, buy TIPS/gold/equities, pay the 30% tax or whatever on the inflationary difference, then buy your stuff. The point is to force you into buying more stable units of account and then taxing the inflation as a "capital gain." Pretty genius because it can be framed as taxing greedy capitalists when literally they're just taxing fractional inflation. |

|

| ▲ | 2 days ago | parent | prev | next [-] |

| [deleted] |

|

| ▲ | asveikau a day ago | parent | prev | next [-] |

| Username is "CS Mastermind". Evidently not an economics mastermind. |

|

| ▲ | jancsika a day ago | parent | prev | next [-] |

| Wait, what's absurd about it? I feel like this is the real-life version of my favorite joke from Andy Kindler: "I know they said don't re-invent the wheel, but does it have to be so round?" Edit: emphasis |

|

| ▲ | imtringued a day ago | parent | prev | next [-] |

| How would that work? You have a claim to a past output that no longer exists. If the nominal value of the claim stays the same, the real value of the denomination unit must change. People don't understand that money is a time and location bound object and pretend it is infinitely liquid and fungible when it isn't. Money is kind of like electricity. When you borrow it into existence and spend it, it travels a path through society, but it must then travel along a return path back to the source. Inflation could be thought of as a form of resistive loss, where current stays the same but voltage drops. There's a reason why demurrage (or its ugly brother inflation) is a necessary bitter pill if you want a working money system. It forces money to travel down the return path sooner than later. |

|

| ▲ | TacticalCoder a day ago | parent | prev [-] |

| [dead] |

{kind=link}