| ▲ | mothballed 2 days ago |

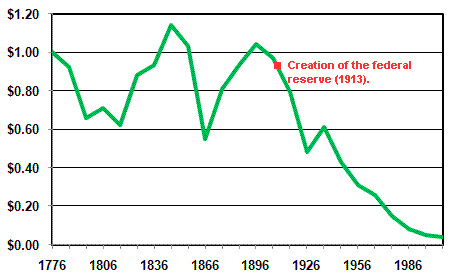

| If you move to before the central bank was created in 1913, the dollar remained remarkably stable in relation, although it did oscillate, it never deviated more than 50% from the starting point until after creation of the fed. https://upload.wikimedia.org/wikipedia/commons/c/c7/Dollar_v... |

|

| ▲ | somenameforme 2 days ago | parent | next [-] |

| What is the source of data that image is using? It seems odd. A datum I quite like is the Campbell's Tomato Soup Inflation Index. [1] Since their introduction in 1897, Campbell's has sold the same tomato soup in the same size container. Its price remained quite stable until 1971 at which point it went into loony land, like many other data. [2] The point is that even after the central bank was introduced, the US remained on a literal or defacto gold standard, of varying sorts, until 1971. That's when Bretton Woods ended and the value of the USD became based on absolutely nothing and the government granted themselves the power to 'print' arbitrary amounts at their discretion. [1] - https://theglitteringeye.com/the-tomato-soup-index/ [2] - https://wtfhappenedin1971.com/ |

| |

|

| ▲ | woodruffw 2 days ago | parent | prev [-] |

| It seems difficult to draw any inference from this, given how different the US’s economy and global position is in 2025 versus 1913. |

| |

| ▲ | gbacon 2 days ago | parent | next [-] | | Lots of topics that we discuss on HN require careful thought and other difficult efforts but somehow do not extinguish our curiosity. Going back to the ancient Romans, an ounce of gold has always been able to purchase a suit of clothes. As the market becomes more efficient at producing goods and services, we should expect prices to decrease, not inflate. In some sectors, we do see this outcome but not in others. Yes, the analysis required to explain why is difficult, and perhaps more difficult is having to face conclusions that challenge one’s priors. | | |

| ▲ | woodruffw a day ago | parent [-] | | There’s a big gap between curiosity and making inferential leaps. > As the market becomes more efficient at producing goods and services, we should expect prices to decrease, not inflate. Yes, that’s why the cost of clothes has decreased in real terms. |

| |

| ▲ | mothballed 2 days ago | parent | prev [-] | | ... I was directly addressing GGP using 1914 as a cutoff. Now you object to the cutoff I didn't introduce only when someone introduce data on the other side of it? Funny how that magically ends up being the case. | | |

| ▲ | woodruffw 2 days ago | parent [-] | | To be clear, I think it’s also hard to make inferences after 1913. But it’s easier (and particularly after 1945, 1971, etc.) because the US’s geopolitical status after those periods is at least analogous and a matter of econometric research. | | |

| ▲ | mothballed a day ago | parent [-] | | The period from 1776-1913 arguably had as many changes as the period from 1913 to 2025. In the first 130 years of the US, the value of the dollar didn't change, as far as I can tell, more than 50% from the starting point. From 1913 to 2025, the dollar lost 96+% of its value. The difference between a ratio of 2:1 and a ratio of more like 30:1. | | |

| ▲ | woodruffw a day ago | parent [-] | | > The period from 1776-1913 arguably had as many changes as the period from 1913 to 2025. I'm not arguing it didn't. But I think in kind the US's global economic position didn't change substantially between full independence in 1783 and 1913. It grew during that period, but the idea of the US as a peer (and then dominant) economic world power is a distinctly post-WWI one. | | |

| ▲ | mothballed a day ago | parent [-] | | Why do you believe that makes the data comparison pre to post central bank irrelevant? |

|

|

|

|

|

{kind=link}