| ▲ | mg 2 hours ago | |||||||||||||||||||||||||

My napkin-math approach to get a bird's eye perspective on the situation: A $1T investment needs to produce on the order of $100B in yearly earnings to be a good investment. Global GDP is about $100T. So one way for things to work out for the AI companies would be if AI raises GDP by 1% and the AI companies capture 10% of the created value. | ||||||||||||||||||||||||||

| ▲ | sottol 35 minutes ago | parent | next [-] | |||||||||||||||||||||||||

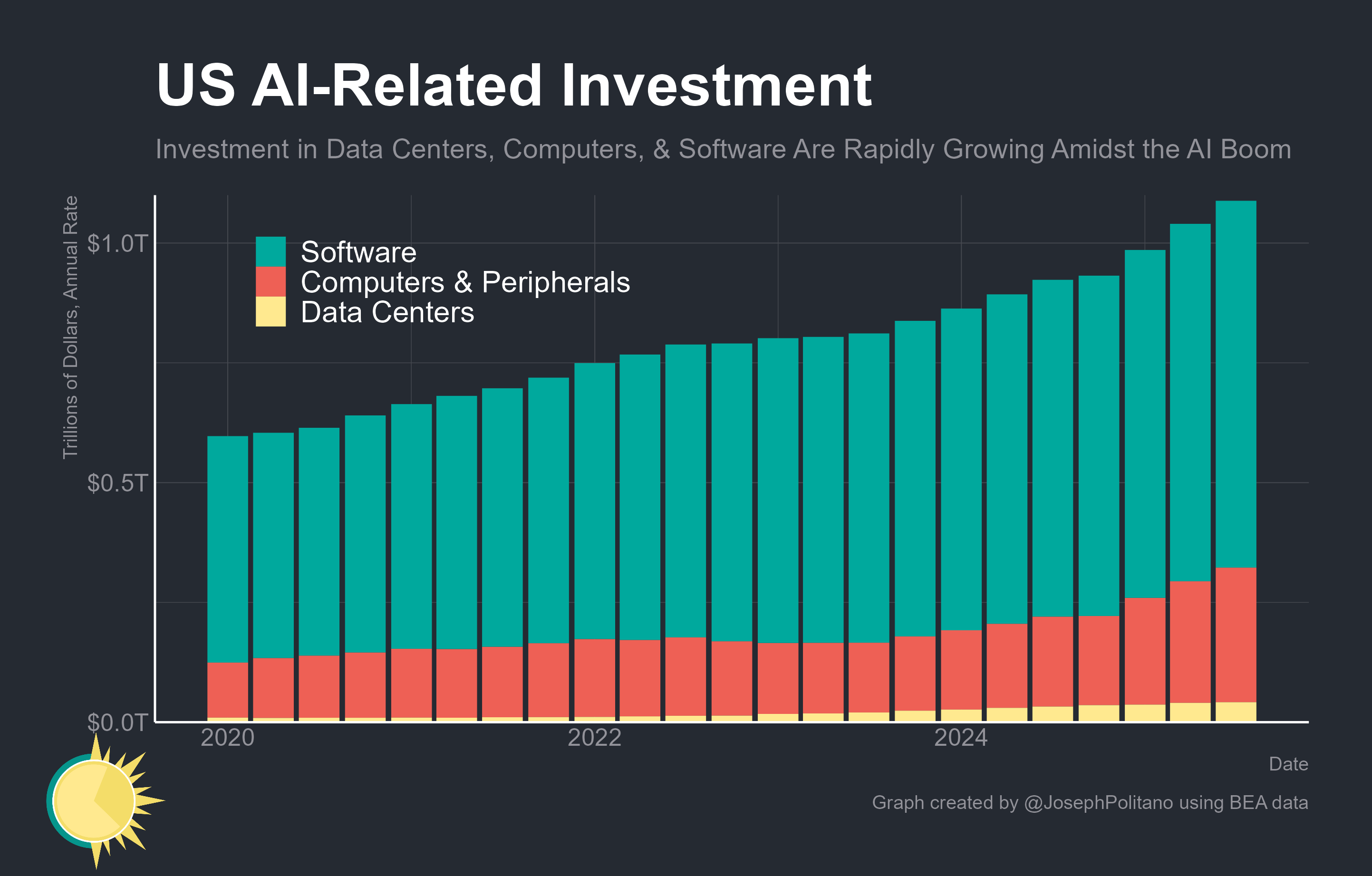

If I'm mistaken, then the article states that the investment is $1T annualized when taking software development costs into account [1] if the labs don't all suddenly decide to stop development. That would mean earnings of ~ $1.1T would be required on that investment annually, so maybe on $2T of revenue, capturing 2% of the global GDP - so I'd estimate that GDP would need to go up more like 5-10% to justify this. [1] https://substackcdn.com/image/fetch/$s_!Gf2t!,f_auto,q_auto:... | ||||||||||||||||||||||||||

| ▲ | louiereederson an hour ago | parent | prev | next [-] | |||||||||||||||||||||||||

At some point AI may deliver the level of net economic benefit you reference, but it's not entirely clear that we're there yet. Right now much of the direct monetization occurs via OpenAI and Anthropic, who together have around $30B in annualized revenue. They are burning cash like crazy, though admittedly have potentially sustainable unit economics (gross margins around 40-60% before revenue share). However, they need to spend a huge chunk of revenue on training. OpenAI spent something like $9b on training against around $13-14b in rev in 2025 (different from annualized rev) according to The Information. Anthropic's mix is supposed to be similar. Also implies a lot (maybe majority) of their compute spend is training. If scaling laws falter, what happens to training spending? What happens to competitive degree of differentiation given Chinese open source models are a few months behind frontier? Then what happens to margins? It is very fragile. | ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ▲ | nradov 2 hours ago | parent | prev | next [-] | |||||||||||||||||||||||||

That reminds me of "Chinese marketing" strategy by a lot of Western companies 30 years ago when their economy first opened up. There are billion people in China so if we can capture just 1% market share there then we'll make a fortune, right? Spoiler alert: it (mostly) didn't work. | ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ▲ | bryanlarsen an hour ago | parent | prev [-] | |||||||||||||||||||||||||

10% capture seems highly unlikely. That level of capture is only possible for b2b high touch sales, aka "call-me" pricing. For call-me pricing to work, you have to ensure that any sort of public sticker price is not a suitable alternative. You can not have a sticker price, make the sticker price so high essentially nobody will buy it or by finding a feature like oauth that makes the public version infeasible for businesses. And then you also have to maintain enough of a monopoly / oligarchy to sustain that level of pricing. I don't think either of those two conditions will apply in the future. AI providers now have a sticker price that provides basically all functionality, almost completely eliminating the opportunity for extremely high-margin b2b. They've decided a small slice of a large pie is bigger than large piece of a smaller pie. I suspect that's true and will continue to be true in the future. An oligarchy is difficult to sustain with more than 3 global players. Right now we seem to have 3 frontier models for coding that can and will charge more than commodity prices. However there are open source non-frontier models that you can use for inference costs only and even if those don't keep up it seems likely there will be enough non-frontier models available that their pricing will also be at the commodity level. Those cheaper models will provide significant downward pressure on frontier pricing. | ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

{kind=link}